What are the catalysts for initiating a pension risk transfer?

Sponsored Content By MetLife

In today’s business world, actively managing a defined benefit (DB) pension plan has become complex and costly. One of the many exceedingly difficult challenges is generating sufficient portfolio returns to fund liabilities in a prolonged low interest rate environment, coupled with market volatility arising from concerns about the Coronavirus pandemic and related variants.

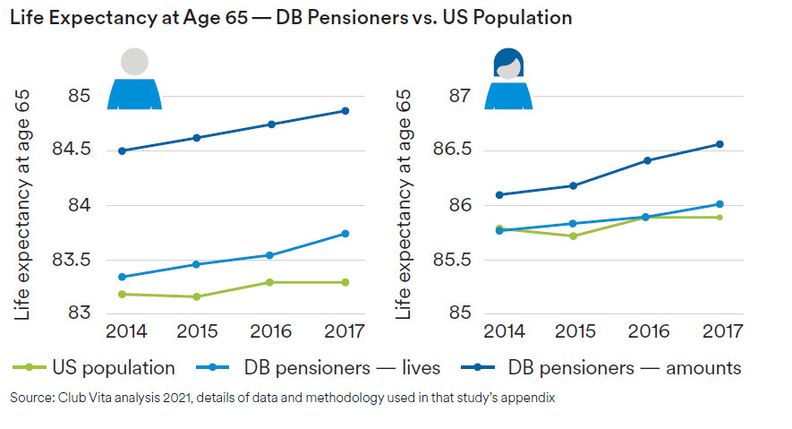

Longevity is also a concern. Pension plan participants are living longer than they have in the past and, according to a recent analysis by Club Vita, mortality rates have been improving much more quickly for U.S. pension plan participants than for other Americans (around 0.8% per year higher among over 65-year-olds).1 Although the final impact of COVID-19 on this population is not yet known, if this pace continues, “the existing [life expectancy] gap between DB pension plan participants and the US population will widen by around 1 more year by the late 2020s.”2 Longevity increases, especially for a very large participant population, can further increase plan costs — making a pension risk transfer (PRT) today all the more attractive.

MetLife has been tracking PRT trends and developments for nearly 20 years. In this latest MetLife Pension Risk Transfer Poll, MetLife commissioned a survey of 253 plan sponsors who have de-risking goals (either near- or long-term) for their pension plan.

1 Club Vita, “Research Note 21-08: Longevity Improvement Rates for U.S. Defined Benefit Plan Participants: Examining Widening Life Expectancy Inequality,” August 2021.

2 Ibid

This sponsored content was not written by the editors of the newspaper, Pensions & Investments, and does not represent the views of the publication, or its parent company, Crain Communications.

Sponsored Content

Partner Content

MetLife

200 Park Avenue, New York, NY 10166

https://www.metlife.com/pensionrisk

Asif Mohamed

Director, U.S. Pensions

(212) 578 8624

[email protected]

Related Content: